While forming regression equation in econometrics, we regularly face various issues with the selection of variable, selection of model and the values of observations. This often leads to challenges on fitting the OLS (Ordinary Least Square) regression. Some of the most common issues faced, the symptom, cause, testing mechanism and remedies are listed here.

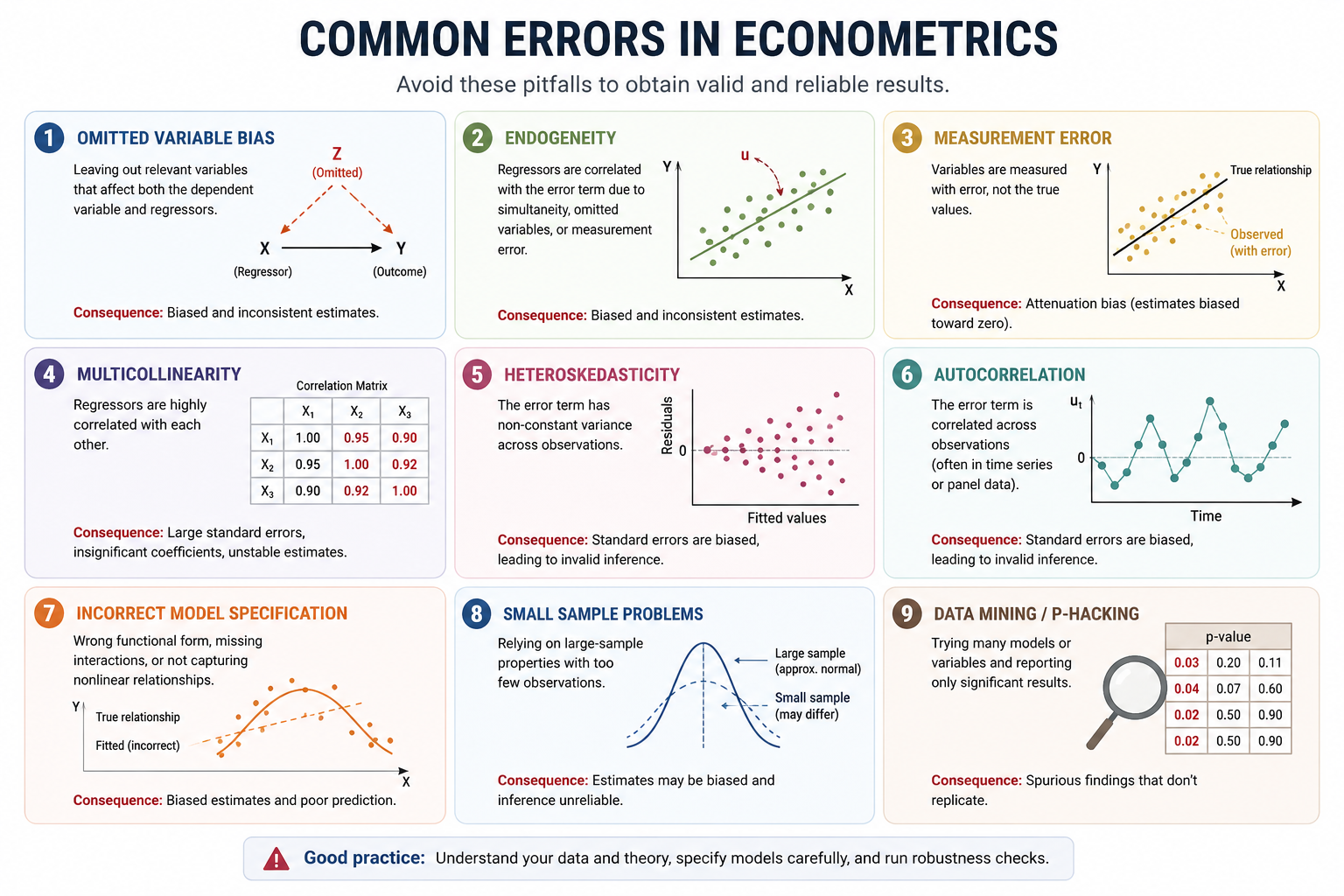

- Heteroscedasticity

- Non constant variance of error term with respect to dependent variable i.e. Var (ui|xi) ≠ σ2

- Cause: Due to scale effect, Omitted Variable, Measurement Error

- Symptom: Fan shaped residuals

- Test: Breusch-Pagan, White, GQ

- Impact: Loss of efficiency of estimator, invalid inference as standard errors are biased, estimators are still unbiased and consistent.

- Remedy: Log transforming the variables

- Autocorrelation (Serial Correlation)

- Error term (ui) correlates with its own past values i.e. Cov(ut, ut-1) ≠ 0

- Cause: Trending data, Omitted Dynamics

- Symptom: Residuals how run/pattern over time

- Test: DW, Breusch-Godfrex, Ljung-Box

- Impact: Inefficient, Invalid Inference but still Unbiased and Consistent

- Remedy: Add lags of the dependent variable

- Multicollinearity

- High Correlation among regressors

- Cause: Similar variables, dummy variable trap, using polynomial forms of same variable (x, x2, x3..)

- Symptom: High R2 but insignificant t-stats, unstable coefficient

- Test: VIF, Correlation Matrix, Conditional Index

- Impact: Inefficient because variance is inflated but still unbiased and consistent

- Remedy: Drop/Combine Variable, Principal Component Analysis, Centering (xi-x¯)

- Omitted Variable Bias

- Missing relevant variable which is correlated with included regressors

- Cause: Data Limits, Poor model specification

- Symptom: Not matching Theory, Coefficient Instability

- Test: Ramsey Reset, Nested Model Comparison

- Impact: Biasedness, Inconsistent, Inefficient, Inferential Invalidity

- Remedy: Add variables, proxies, Instrumental Variables

- Endogeneity

- Covariance between error term and dependent variable Cov(X,u)≠0

- Cause: Simultaneity, Omitted Variable, Measurement Error

- Symptom: Reverse causality suspicion, implausible coefficients

- Test: Hausman, Durwin-Wu-Hausman

- Impact: Biased, Inconsistent, Inefficient estimate, invalid inference

- Remedy: Instrumental variable, fixed effect models, control function

- Non Normal Errors

- Errors are not normally distributed

- Cause: Outlier observations, skewness, model misspecification

- Symptom: abnormal histogram, Q-Q Plot

- Test: JB, Shapiro-Wilk

- Impact: Invalid inference for small sample size

- Remedy: Transform data, remove outliers, increase sample size

Note: This list is not exclusive and some contents are generated from AI.